Two frequently conflated definitions in the ‘startup ecosystem’ are that of a small business (I often say SME, meaning small to medium enterprise) and a startup.

It’s hard to wrap your head around what the differences are, and while there are some frequent offenders (cough, government, cough), I’ve also seen the same misunderstanding by founders, professional advisors and even investors.

At the core, startups are high growth, high-risk businesses designed to go big or die.

Small businesses are usually lower risk (albeit not universally) and have a lower return profile to go alongside that. Small businesses often do not grow as quickly as startups either. Sometimes a startup turns out to be a small business in disguise over the long run, which can be good or bad.

Let’s look at some of the common traits of the two.

Startups

High growth. In the early days, you expect huge growth month-on-month.

High risk. Most of the time, they die. They don’t struggle along, they just die.

Go big or die. If successful, a startup becomes Atlassian, Facebook or Google (or exits along the way). If not successful, it goes to zero and everyone is unemployed.

You will notice the criteria does not include ‘new’, ‘young’ or ‘has table tennis tables in the office’. I would argue a startup is ‘small’, but that is a relative term. (Is Facebook a startup? No. Uber? Very unlikely in my opinion. They once were, but once you’re listed that somewhat makes you not a startup anymore.)

A commonly cited post (not without its critiques) is Paul Graham’s Startup = Growth article.

Small businesses

Do not grow as quickly. While not impossible (it’s easy to three times from $1 in revenue), you don’t see them grow as quickly (or expect them to).

Less risky. Opening a bar where there is no foot traffic is obviously a huge risk (let’s be honest, it’s stupid), but the paths are usually more well-worn about how to minimise risk.

Have a natural asymptote of size. Unlike startups, small businesses often lack scalability, so they will always have a natural ‘top’ of what they might achieve. You might start opening multiple locations or franchise the model, of course, but these are workarounds rather than core to the model, and each ‘location’ or franchise has the same natural limit.

A successful startup is no more or less of a ‘success’ than a successful small business. On the whole, small businesses employ vastly more people, pay more tax, and last longer than startups, which have a very long tail.

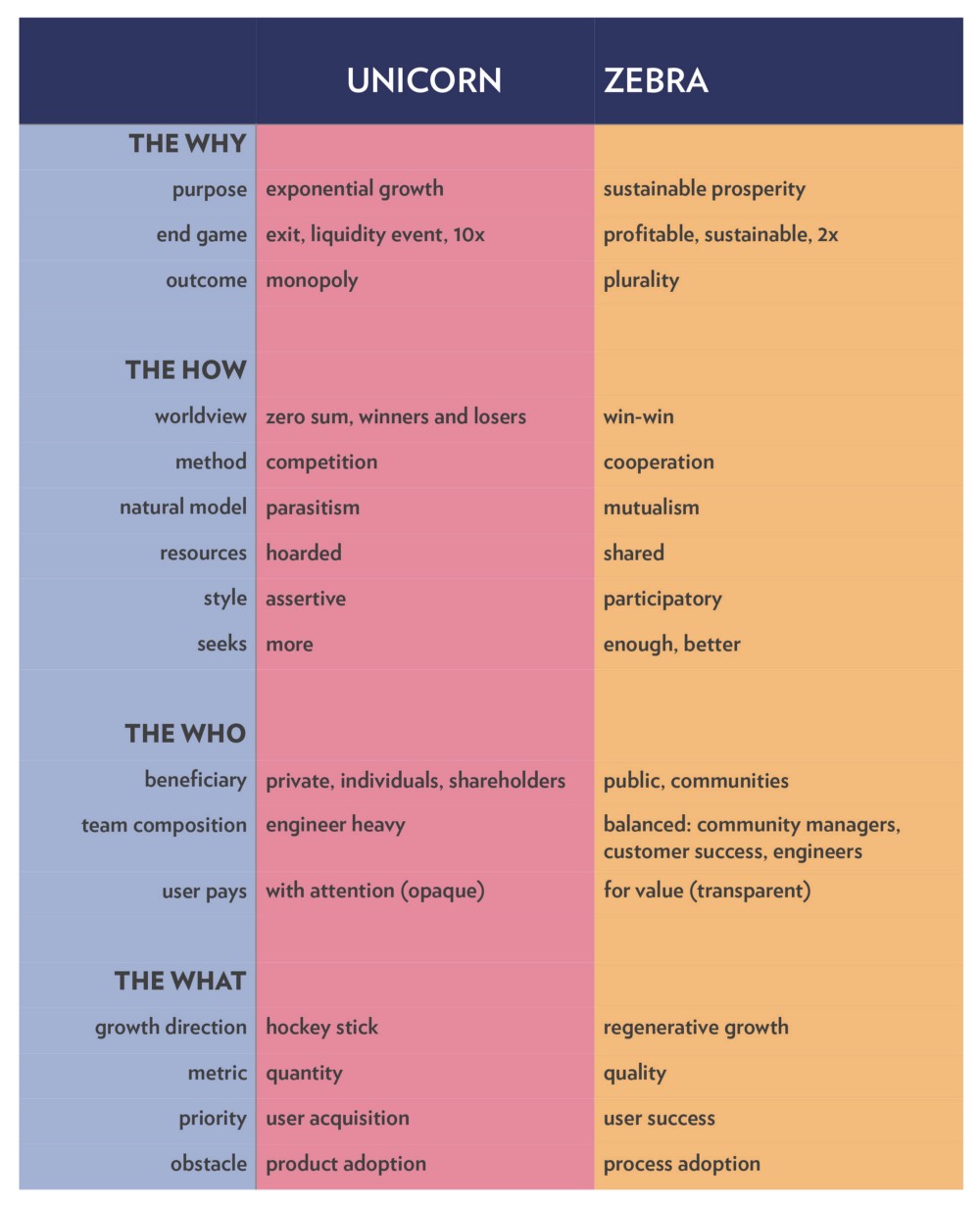

A good post about this distinction is titled “Zebra companies offer an alternative to the unicorn fantasy“. From the article, here’s a table comparing ‘unicorns’ (startups) and ‘zebras’ (small businesses).

Small businesses are usually inherently more profitable at a similar age. Few small businesses can afford to continually run at a loss. The decision to build a company to be profitable is very different from building one to be big. This is not to say they are incompatible in the long run, but you need to decide where you are going to guide yourself in the shorter term.

I find it hard when I see a founder who has a great small business idea who tries to turn it into a startup. Not all things need to have fuel poured on them by venture capitalists to see if they 1000x in 10 years or burn to a crisp. Having a company that is profitable, small, simple to manage and gives you new challenges every day is just as fulfilling, and probably better for you in the long run than trying to swing for the fences.

Of course, not everyone is happy with acknowledging they have a small business and not a startup — and that’s okay! This might not be your high-growth crazy unicorn startup, it might be your first learning ground. Or you might just need to normalise into acknowledging having a small business that makes money can be fulfilling and let you actually live a life not full of meetings with venture capitalists.

Small businesses aren’t just cafes and bars (they make it easy to compare the two of course), but also tech companies! But more on that later.

Supporting startups and small businesses

So how do you support startups and small businesses? Governments, in particular, want to support them both, and often try and call them both ‘startups’ for the purpose of seeming innovative and in touch with our ‘new economy’.

But their needs are different. Small businesses don’t need ‘paths to capital’, and encouraging founders to go and look for it will only create more small businesses funded like startups, which usually ends extremely badly for everyone involved.

Both have some core requirements. Founders (of both) need to understand the basics of accounting, tax, the law and things such as HR or ‘people skills’. These are table stakes for running any company, startup or not.

Controversial view: startups don’t need to be thoroughly lectured about how to pitch for money. That is not a success metric and we need to stop using it as one. Our ecosystem is at the stage where a VC can usually tell the difference between a great company pitched poorly and a terrible company pitched well. Governments funding these programs irritate me endlessly, particularly when the people teaching have sat on neither side of the table before.

Beyond those core requirements though, putting the two in a room won’t help. They don’t speak the same language.

It is ballistically insane to a small business founder (‘owner’) to see VC-funded startups losing millions each month and acting like they’ve been incredibly successful.

And a startup founder doesn’t understand why you wouldn’t 10x your company every year and ‘gun for growth’, instead focusing on building a low(er) risk business that can provide ongoing cashflow (profit) for the founder, their family and employees (and theirs).

A brief personal aside: why I have a small business (that is kind of turning into a startup)

I often have to answer this question about my company, Schedugram.

When I started it back in 2012, I figured we might turn over $1 million if successful, and that would be our natural asymptote. We’d have two-five employees (definitely no more than 10), and last for a year or so. We have grown a lot bigger than that, in revenue and people. We just signed our 23rd full-time employee, and 4.5 years down the track, our annual revenue is a lot more than $1 million.

It was built as a small business, for strange reasons that aren’t the point of this post, but meant it was a ‘bootstrapped startup’ (which usually means it’s a small business), inclusive of things like ‘the company has to be profitable because I’m not a bank’. I honestly thought nobody would be dumb enough to invest in my company.

We live in an awkward middle space. We aren’t growing 300% year-on-year (but we’re still growing year-on-year), and have a scalable business model that is profitable at its current scale and supports our global team of employees and contractors.

Galileo co-founders James Alexander and Hugh Stephens. Source: Supplied.

Looking back, it probably could have been a ‘startup’, with the whole ‘go raise money’ thing. That would have changed some of the decisions I’ve made for better or worse. For example, it would have allowed us to have more resources earlier, rather than scale until everyone rips their hair out, then hire, then scale, then hire. It would hopefully have given me connections to insights that I didn’t (still don’t) really have, and give me people to be accountable to, plus occasionally be my cheerleader.

Sometimes it’s hard though. You read in the news about these companies that are doing 10% of your revenue and losing a few million a year, but apparently valued at $50m and they’re heralded as a ‘huge success story’.

It took a lot of time to realise raising money is a stop on a journey, not a successful destination — and valuations are bullshit until they’re liquid and realised. I tell people that even now, but still have to stop myself from falling into that trap.

We’re kind of pivoting from small business mode into startup mode now, as we take on the next big phase of growth and new challenges. It may not work — I may end up killing the goose that lays the golden eggs — but it’s what I think the company and our customers need to stand the test of time.

Investors in small businesses and startups need different expectations

One other thing people need to understand is what an investor expects from a small business compared to a startup. Investors exist for cafes too — just not series B or C investors, but small businesses can also be capital intensive at certain stages.

When you invest in a small business, you expect the company to eventually pay you back slowly over time. Indie.vc is a good example of how you might do this institutionally, but it might be parents, friends, family or fools (or angels) who are happy to receive small dividends over time from a profitable small business. And that’s fine! You are also taking less risk for your capital, and your returns might be great over the long run but you aren’t likely to get $2.5m in six years back for your $25k.

When you invest in a startup, it usually has to hit it out of the park (1000x return) or it goes to zero. This is why startup investing is best done in portfolios — if you could identify the two or three businesses likely to 1000x and avoid every other promising sounding startup, please give me a call. But for most of us, you need to ‘spread your risk’ across different startups in the hope that you’ll get the big ones.

This is the ‘power law’ of (startup) investing, and you can read a good mathematical take about it here and here. What it means though is that your regular venture capital fund needs to find companies to hit that power law. They don’t want companies that return small amounts of money every year, forever. They want companies that will smash it out of the park, and while some might return little bits of money (one-three times what they put in), it’s the one or two that return 20-1000 times that actually ‘return the fund’. Pitching an investor like this a business that is likely to have a return profile of a small business will not be relevant to what they need to be successful.

I invest in some things that look like small businesses, and some things that look like startups. Usually there’s a chance they can change from being a startup to a small business if something doesn’t work out (this is the advantage of cashflow), and I don’t need my returns to fall within a 10-year-fund lifecycle, so if I get paid $5000 every year for 30 years I’m happy enough. Sure, $150k now is better if that’s a choice though.

Understanding categories and stages is how to help

Finally, the combination of understanding categories (startups versus small businesses) as well as stages (in B2B SaaS, you do $0-1 million annual revenue, $1-10 million, $10-100 million and then $100+ million) is needed for you to work out how to support companies.

When I go to a conference full of people talking about $0-1 million, it’s not helpful. Similarly, the person who is the vice=president of operations at a company doing $100+ million is an interesting and perhaps inspiring story, but not really able to be relevant to us right now. Someone running a product team of 20 people at Google (with 62,000 employees) isn’t going to be able to give me much more than some principles to apply if my product team is two, with 25 employees.

The good speakers at events know how to distil what they can to the stage of the audience, the bad ones think that their experience is universally applicable regardless of context.

Governments fund a lot of ‘$0-1 million’ staged events and courses. To be fair, the majority of founders are there — it’s a very bottom-heavy pyramid distribution. But ironically, if the output is ‘we want more people employed’, doing a better job supporting small businesses or startups at the next stage (critically, $10-100 million, which is when you often see companies move headquarters overseas) would have a much better outcome.

What I’d like to see is more events segmented to different company stages, and more honesty about what stage a startup is at (and thus who should attend). There is nothing more frustrating than seeing someone at $0-1 million who thinks they’re at $1-10 million. Even at $1-10 million, you are not necessarily at ‘product/market fit’, and you definitely won’t be with a $1 million run rate.

This post first appeared on Hugh Stephens’ blog and was republished with permission.

NOW READ: How to secure a government grant for your small business or startup

NOW READ: Growing pains: The stress of success in small business

COMMENTS

SmartCompany is committed to hosting lively discussions. Help us keep the conversation useful, interesting and welcoming. We aim to publish comments quickly in the interest of promoting robust conversation, but we’re a small team and we deploy filters to protect against legal risk. Occasionally your comment may be held up while it is being reviewed, but we’re working as fast as we can to keep the conversation rolling.

The SmartCompany comment section is members-only content. Please subscribe to leave a comment.

The SmartCompany comment section is members-only content. Please login to leave a comment.