Source: Getty.

In 2020, the global economic landscape was shaken by the COVID-19 pandemic. Here in Australia, borders closed to international visitors, social-distancing measures were invoked and working-from-home became the norm.

But despite the dramatic impact of COVID-19, there has been a surge in the number of Australians realising the ‘great Australian dream’ of homeownership.

With record low interest rates, massive fiscal stimulus from governments, and explicit measures targeted at supporting the construction sector (namely the HomeBuilder scheme), the housing market in 2020 defied expectations of a large downturn.

In July 2020, the number of new home loans provided to first-home buyers exceeded 10,000 for the first time in 10 years.

This increase has continued unabated, with new home loans to first-home buyers exceeding 14,000 in November. Excluding loan refinancing, over 35% of new owner-occupier loan commitments were for first-home owners.

Recent survey data suggests this trend is likely to continue in the short term. Longer-term, however, the research suggests that affordability issues that are locking people out of the market will continue.

Back in April 2020, amid the onset of the pandemic, the market was anticipating a sharp drop in property prices.

The Melbourne Institute’s Time to Buy a Dwelling Index, which measures consumer sentiment towards purchasing dwellings, plummeted to 82.1. An index value of 100 represents the point at which optimists exactly offset pessimists, with values below 100 indicating that pessimists outweigh optimists.

At that time, over 30% of consumers expected house prices to fall by up to 10% over the next 12 months.

By December, however, the Time to Buy a Dwelling Index had dramatically recovered to pre-COVID levels, with only 8% of consumers expecting prices to fall by up to 10%.

Currently, over 40% of consumers now expect prices to increase by up to 10% over the next 12 months.

The pace of house price appreciation has been inordinately sharp over the past few years, outpacing income growth and making housing less affordable — especially for lower-to-moderate income households.

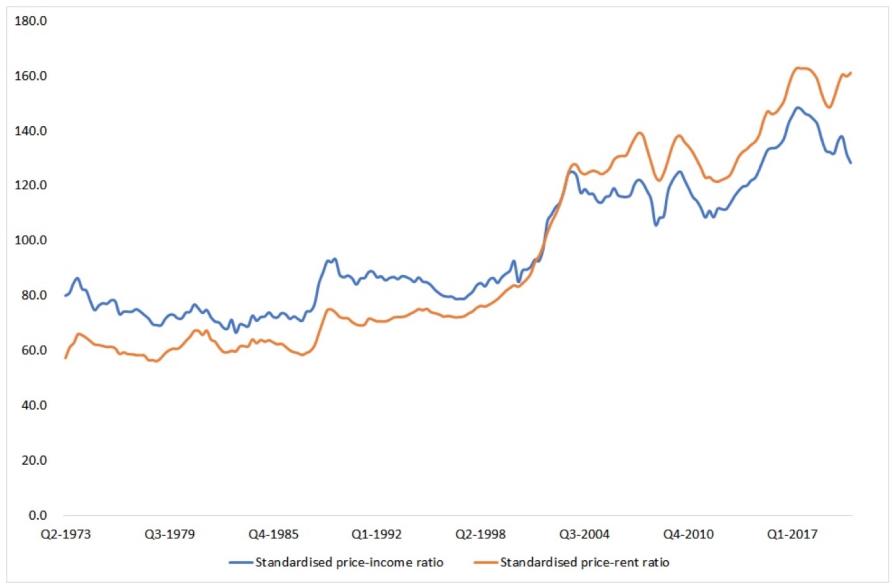

The deterioration in housing affordability is highlighted in data compiled by the OECD showing a sharp increase in Australian house price-to-income and house price-to-rent ratios, particularly over the past 20 years (see graph below).

The house price-to-rent ratio is a measure of the strength of the housing market relative to rental markets — the higher the ratio the more house prices are outpacing rents.

In the 1970s and 1980s, the OECD’s house price-to-income ratio averaged around 76 for Australia, rising to an average of 85 during the 1990s. The ratio surpassed 100 for the first time in 2002 and, over the past five years, has averaged nearly 140.

Unsurprisingly, given the increasing number of people being priced out of housing, since the mid-90s, the proportion of renters has risen from below 20% in New South Wales and Victoria, to approximately 30%.

This increase in the supply of rental properties has been largely driven by ordinary households, with one-in-five Australian households owning more than one property, and about 5% of households owning four or more properties.

Notwithstanding the increase in first-homeownership and home-buyer sentiment that we have seen during 2020, it’s unlikely that these broader trends, particularly the rising proportion of renters, will change.

A graph of OECD data showing how Australian house prices have been outpacing incomes and rents. Source: Melbourne Institute.

The improved housing market sentiment is far from uniform across different demographic groups. It is stronger among those who already own a house that they can therefore sell or borrow against to easily buy again, but more muted among renters lacking these advantages.

Broken down by age, housing sentiment is strongest for older Australians, a group that is more likely to own their home, and weakest for Australians aged 18-34 years who are more likely to be renting than their older counterparts.

Previous research with my colleague Professor Guay Lim has highlighted the importance of monetary policy and interest rates on house prices and the potential for the housing market to overshoot on prices.

Although low interest rates should naturally lead to higher asset prices because buyers have access to cheaper credit, our work suggests that households can over-react to low interest rates, leading to greater than expected house price rises, particularly in larger capital cities.

Low interest rates are, therefore, more likely to result in two-speed housing markets.

Recent research has also provided evidence that house prices in more expensive areas are often more sensitive to changes in interest rates, with lower interest rates potentially resulting in greater housing wealth inequality.

The research suggests then, that expectations of a significant downward correction in house prices that will favour lower-income, first-home buyers are unlikely to be realised.

Importantly, the presence of record low interest rates (coupled with Reserve Bank’s guidance of a prolonged period of low interest rates) is likely to support house prices in the short to medium term — notwithstanding lower population growth going forward.

This suggests that existing homeownership trends are likely to continue to persist, with large numbers of younger households continuing to rent rather than having the ability to purchase their own homes.

In this environment, it’s vital that policies support renters and facilitate an environment of sustainable long-term renting, particularly with regards to normalising longer-term rental agreements.

The reality is that many more Australians will be long term renters, and policymaking needs to adapt accordingly.

This article was first published on Pursuit. Read the original article.

This article is supported by the Judith Neilson Institute for Journalism and Ideas.

ABOUT THE AUTHOR

Handpicked for you

HomeBuilder leads to spike in material and labour costs, hitting smaller builders where it hurts

COMMENTS

SmartCompany is committed to hosting lively discussions. Help us keep the conversation useful, interesting and welcoming. We aim to publish comments quickly in the interest of promoting robust conversation, but we’re a small team and we deploy filters to protect against legal risk. Occasionally your comment may be held up while it is being reviewed, but we’re working as fast as we can to keep the conversation rolling.

The SmartCompany comment section is members-only content. Please subscribe to leave a comment.

The SmartCompany comment section is members-only content. Please login to leave a comment.